WHAT LEADERS NEED TO KNOW

- The issue — the cost of capital has reset upward and settled there; the cheap-money base case that underwrote a decade of decisions is gone.

- The risk — a wall of low-coupon debt is maturing into a 5%-plus market, hurdle rates built on free money are silently mispricing capex and deals, and central banks are diverging.

- The opportunity — firms that reprice the hurdle rate early, map their maturities and fund regionally can allocate capital with a discipline rivals have lost.

- The decision required — re-underwrite every live capex and M&A model on a higher-for-longer cost of capital, and build refinancing optionality now.

- The timeframe — the repricing is already underway as cheap pandemic-era debt (issued in 2020–21) reaches maturity; the next 24 months are the crunch.

Everyone is watching the wrong number

When the cost of capital comes up, the room turns to the central bank — did the Fed cut, will the ECB, where next for Bank Rate. That reflex is now a trap. The policy rate is the least of it. The real repricing is happening quietly on the balance sheet, as a decade of cheap debt matures and rolls over at coupons that would have looked punitive in 2021. For anyone tracking Global Economy & Policy, the cost of capital has reset — not for a cycle, but as the base case. This cluster sits under our pillar guide, The Benign Backdrop Is Over, and takes one of its four forces — capital — down to the decisions you make this quarter.

Key signals

- Rates settled high, not back. The Fed held its target range at 3.50–3.75% in June 2026; the Bank of England held Bank Rate at 3.75% (Federal Reserve, June 2026; Bank of England, June 2026).

- Central banks are diverging. The ECB moved the other way, raising its deposit rate to 2.25% with effect from 17 June 2026, so “the cost of capital” now depends on where you borrow (ECB, 2026).

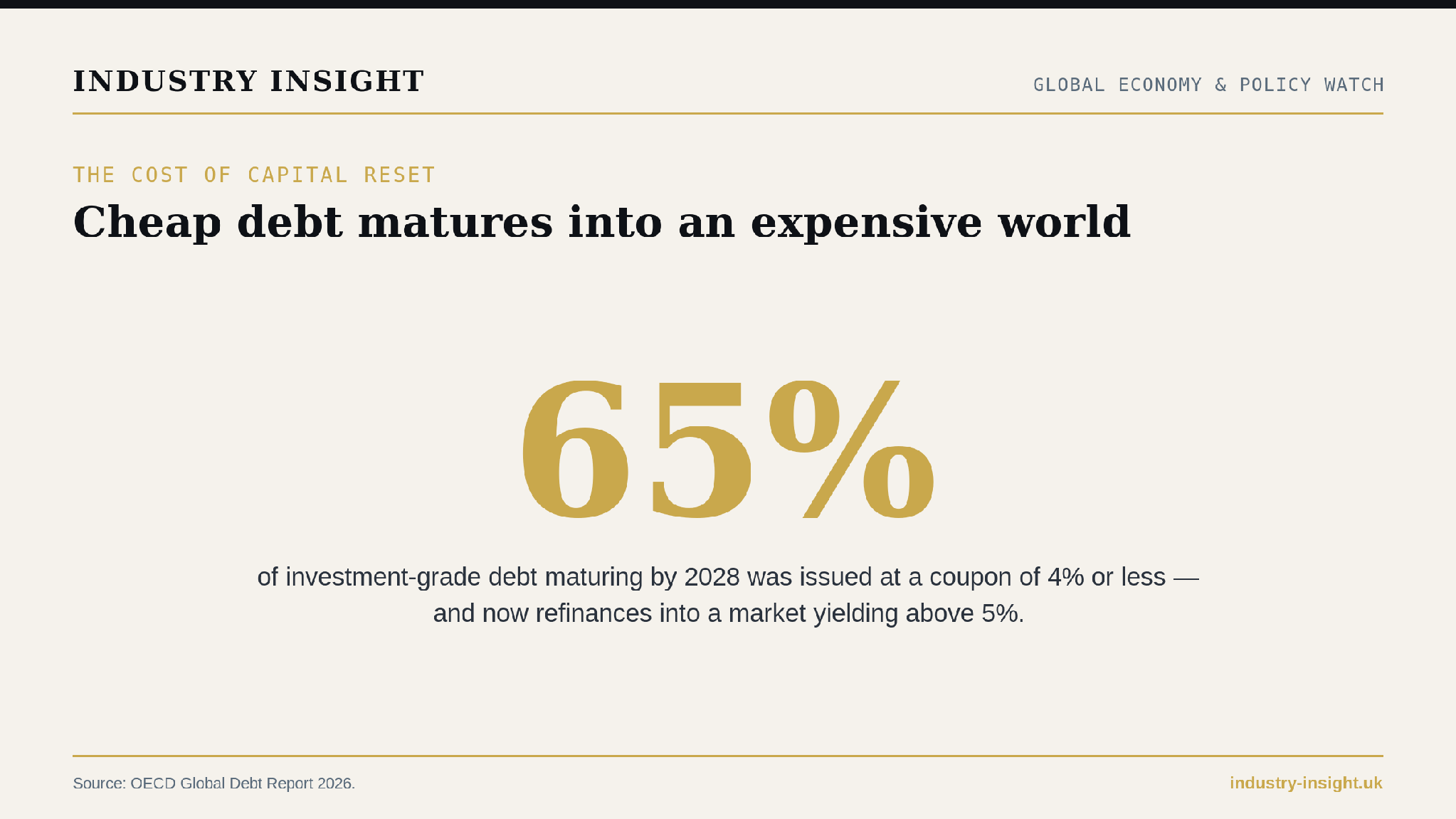

- The refinancing wall reprices upward: 65% of investment-grade debt maturing by 2028 was issued at a coupon of 4% or less, and now rolls over materially higher (OECD Global Debt Report 2026).

- The volume is front-loaded. About 24% of outstanding investment-grade debt and 31% of sub-investment-grade debt falls due within three years (OECD, 2026).

- Credit is priced for perfection. Investment-grade spreads sit around 74 basis points — near their tightest in decades — even as all-in yields hold above 5% (ICE BofA index data, mid-2026), leaving little cushion if conditions turn.

The step-up is arithmetic, not a forecast

Central-bank watching distracts from the mechanical squeeze already in train. Between 2020 and 2021, companies termed out debt at the cheapest rates in modern history. Those bonds are now maturing into a market where investment-grade yields sit above 5%. The OECD's finding is the one to sit with: 65% of investment-grade debt due by 2028 carries a coupon of 4% or less. Refinancing it is not a choice, and the step-up is not a projection — it is arithmetic. Even if policymakers hold or trim rates from here, interest costs still rise as the old stock rolls, quarter after quarter. This is a slow, certain drag on cash flow that has nothing to do with the next rate decision and everything to do with the last five years of issuance.

Figure 1. The refinancing wall only reprices one way (Source: OECD Global Debt Report 2026).

There is no longer a single cost of capital

For most of the last decade, easing moved in near-lockstep, and a treasurer could treat global funding as one pool with one price. That assumption has broken. In June 2026 the Fed and the Bank of England held while the ECB raised — a genuine divergence, driven by different inflation and growth positions. Where you raise capital, in what currency, and against which curve is now a live strategic decision rather than a plumbing detail. Hedged funding costs, regional spreads and the timing of local issuance windows can move the all-in number by more than the headline policy rate does. The single global cost of capital is a relic of the synchronised-easing years.

The hurdle-rate reset is permanent

The deeper change is behavioural. A risk-free rate that actually pays reintroduces discipline that a generation of managers never had to practise. Every capex case, acquisition and buyback now competes against a genuine alternative return, and projects underwritten on a sub-3% risk-free rate simply do not clear at a 7–8% WACC. This is analysis rather than a published figure, but the direction is not in doubt: valuations compress, payback periods shorten, and marginal projects that used to squeak through no longer do. The firms that struggle will be the ones still running live models on a hurdle rate quietly inherited from the cheap-money era. Repricing that number is the single highest-leverage move a finance function can make this year.

What leaders should do now

Next 7 days

Pull the maturity schedule. Know exactly what debt rolls over the next 24 months and the coupon step-up on each tranche, so the refinancing drag is a number on a page rather than a surprise in a results call.

Next 30 days

Re-underwrite the hurdle rate. Raise the WACC assumption in every live capex and M&A model to reflect higher-for-longer, and re-run the pipeline. Projects that only clear on cheap-money maths should be paused or killed now, not after they have absorbed capital.

Next 90 days

Build financing optionality. Stagger maturities so you never have to refinance a large slug into a single bad window, diversify funding sources and currencies given central-bank divergence, and lock terms where the curve lets you.

Three boardroom questions

- What is our weighted refinancing step-up over the next 24 months, and can operating cash flow absorb it?

- Have we re-underwritten our hurdle rate, or are live models still discounting at a cheap-money WACC?

- Given central-bank divergence, are we raising capital in the right markets and currencies?

Five strategic takeaways

- Reprice the hurdle rate now. A WACC inherited from the cheap-money years is mispricing every decision that crosses the board table.

- Map the maturity wall. Quantify what rolls and the step-up before it lands, not after.

- Fund regionally, not globally. Divergence means where and in what currency you borrow is now a strategic call.

- Stagger and pre-fund. Maturity optionality is what stops you refinancing into a hostile market.

- Kill the zombies. Returns that only ever worked at 2% money do not belong in a 5%-plus world.

Reprice before the market does it for you

Cheap money is not a delayed train; it has left the station. The firms that win the next few years are the ones repricing early. They raise the hurdle rate and map the maturities. And they stop funding projects that only ever worked because capital was free. Reprice your decisions before the market does it for you.

Explore the Global Economy & Policy series

This cluster sits under Global Economy & Policy, alongside the pillar cornerstone and its companion clusters:

- The Benign Backdrop Is Over: The 2026 Economy (pillar)

- The Hormuz Shock: The 2026 Oil Crisis as a Commercial Risk

- Europe's Digital Rulebook Hardens: DMA, AI Act and Sovereignty

More clusters publishing soon: Energy Volatility and the New Cost Base · The Geopolitical Risk Map for Leaders.

FAQs

Will the cost of capital fall back to pre-2022 levels?

Unlikely any time soon. Policy rates have settled well above the 2010s average, and the OECD notes corporate interest costs keep rising as cheap debt refinances. Treat higher-for-longer as the base case, not a temporary peak.

What is the “refinancing wall”?

The concentration of low-coupon debt issued in 2020–21 that is now maturing. The OECD finds 65% of investment-grade debt due by 2028 carries a coupon of 4% or less, so rolling it over means a material step-up in interest cost.

Why are central banks diverging?

Different inflation and growth positions. In June 2026 the Fed and the Bank of England held rates while the ECB raised, so borrowing costs now vary by region and currency — a change from the synchronised-easing years.

What should a CFO do first?

Pull the maturity schedule, quantify the refinancing step-up over the next 24 months, and re-underwrite the hurdle rate in every live capex and M&A model.

Sources:

Federal Reserve FOMC statement (17 June 2026); Bank of England Monetary Policy Summary (June 2026); European Central Bank monetary policy decisions (June 2026); OECD Global Debt Report 2026; ICE BofA US Corporate Index data (mid-2026). Figures should be re-verified against the latest source at publish.