Data accurate as of 01 July 2026.

WHAT LEADERS NEED TO KNOW

The Issue

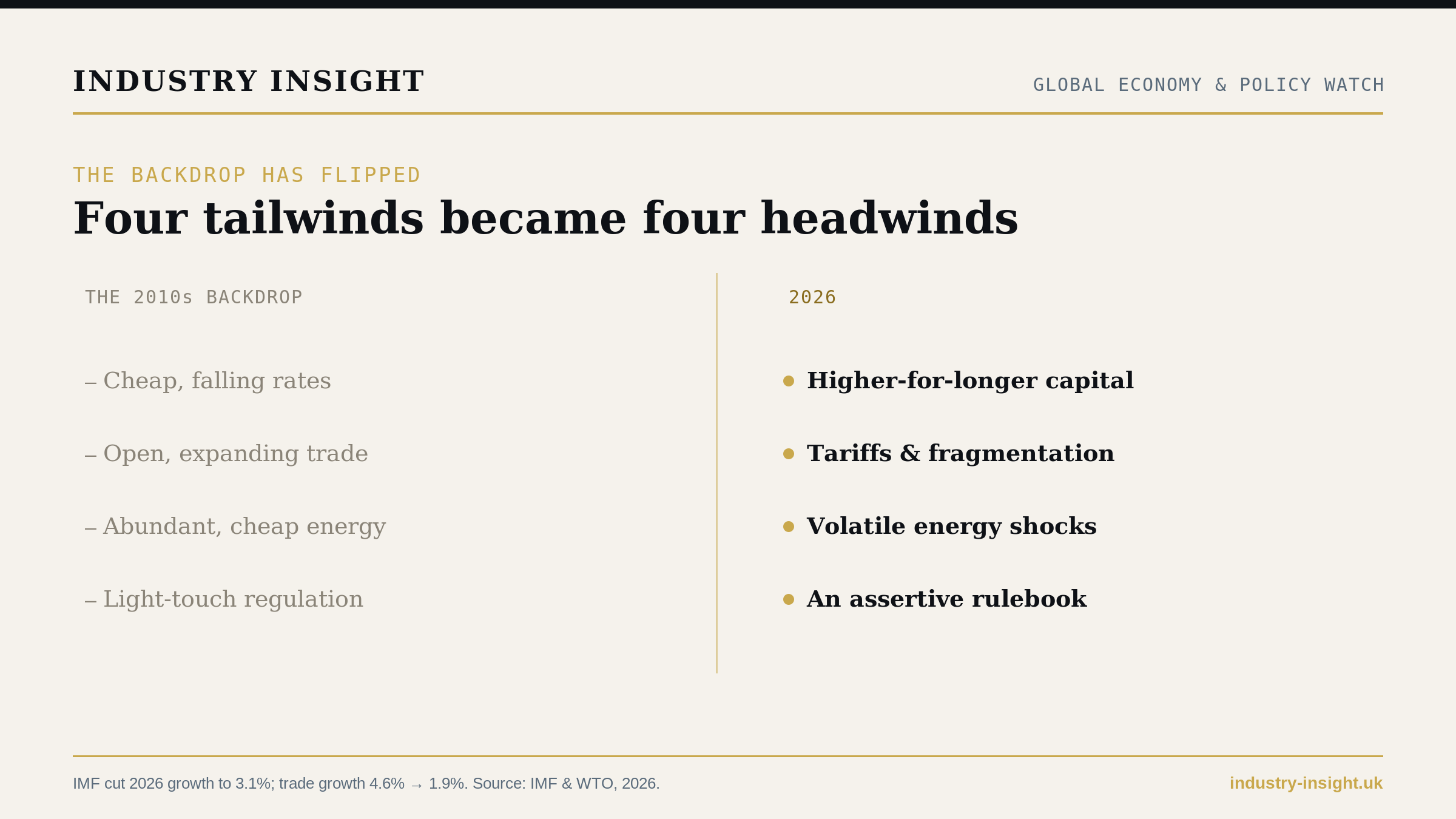

The four conditions executives could once treat as a stable backdrop — cheap capital, open trade, cheap energy, light regulation — reversed at once.

The Risk

Growth is downgraded (3.1%), inflation is up (4.4%), the cost of capital is structurally higher, trade is fragmenting, and downside risks dominate.

The opportunity

Companies that treat macro and policy as planning inputs, not headlines, can price risk, secure resilience, and move while rivals freeze.

The decision required

Build scenario planning, balance-sheet resilience, and a policy-and-macro watch function into how you run the business.

The timeframe

This is the operating environment now, not a passing storm.

The weather changed. Most strategy decks did not notice

Somewhere in the last two years, the weather changed, and most strategy decks did not notice. For fifteen years, the macro environment behaved like a tailwind nobody had to thank: money was nearly free, trade kept widening, energy was cheap and abundant, and regulators mostly stayed out of the way. You could plan on autopilot, and the world would cooperate.

For anyone tracking Global Economy & Policy, the single most important fact of 2026 is that the autopilot is gone: all four tailwinds turned into headwinds at once. The IMF has cut global growth to 3.1% and pushed inflation back up; capital is dearer and staying that way; trade growth has collapsed from 4.6% to 1.9%; and energy and regulation have become things that can blow a quarter apart. Policy has stopped being the backdrop to strategy and walked onto the stage. The instinct is to wait for the old normal to return; it will not, and waiting is the expensive mistake. This guide maps the new weather — and what it asks of the people who must plan in it.

Key signals

- Growth down, inflation up — the IMF cut 2026 global growth to 3.1%, from a pre-conflict 3.4%, and raised headline inflation to 4.4% (IMF, April 2026).

- Capital is structurally dearer — central-bank rate cuts are coming slower and shallower than markets banked on, keeping financing costs elevated; the IMF warns an escalation would push corporate risk premiums up a further 100–200 basis points (IMF, 2026).

- Trade is stalling — merchandise trade growth is set to slow to 1.9% in 2026, from 4.6% in 2025 (WTO, 2026).

- Investment is pulling back from exposed sectors — greenfield project numbers in tariff-exposed, value-chain-intensive sectors fell about 25% in 2025, even as overall global FDI rose (UNCTAD, 2026).

- Downside risks dominate — wider conflict, deeper fragmentation, an AI-expectations reset, or renewed trade tensions could each weaken the outlook further (IMF, 2026).

The four forces that reversed at once

1. The cost of capital

Higher-for-longer is the new baseline. Firmer inflation expectations and tighter financial conditions mean the rate cuts markets banked on are coming slower and shallower than assumed — and the IMF warns a further escalation would add 100–200 basis points to corporate risk premiums. Every capex case, acquisition, and growth plan now has to clear a higher bar.

2. Trade and tariffs

Globalisation has given way to fragmentation. Merchandise trade growth has fallen from 4.6% to 1.9%, tariffs are being used as strategic and industrial tools, and greenfield investment in exposed sectors fell by about a quarter in 2025. By UNCTAD's measure, nearly two-thirds of world trade sits in value chains now being actively reshaped by geopolitics.

3. Energy

Volatility has become structural, not episodic. The 2026 Hormuz shock pushed Brent into a $93–105 band and reordered shipping and inflation — a live commercial risk for anyone who uses energy or moves goods, as we cover in The Hormuz Shock.

4. The regulatory state

Light-touch is over. From the EU's hardening digital rulebook to tariffs wielded as policy, the state is now an active force in markets, detailed in Europe's Digital Rulebook.

Why it matters: they compound

Here is what makes 2026 genuinely hard, rather than merely gloomy: the four forces do not queue politely. They reinforce one another. Picture a single overseas plant expansion — financed at a higher rate, built into a tariff-exposed supply chain, powered by volatile energy, and selling into a tightening regulatory regime. That is four hits in one decision, and the interactions are worse than the sum of their parts. The benign decade let companies run lean on resilience and scenario planning; 2026 is the bill arriving.

Figure 1. The macro backdrop has flipped — four tailwinds became four headwinds (Source: IMF & WTO, 2026).

Who is exposed

Anyone who allocates capital, expands, or runs a cross-border supply chain — which is to say, almost every serious business. Capital-intensive and globally-exposed firms feel it most acutely. But the most dangerous position is a mindset: treating macro as the economists' problem and policy as someone else's department. In 2026, that is how plans quietly break.

What leaders should do now

Next 7 days. Re-underwrite the plan against the new baseline — higher cost of capital, slower trade, volatile energy, and active regulation. Find where one old assumption (cheap money, open trade, cheap energy, or light regulation) is still silently baked in.

Next 30 days. Bring scenario planning back; it lapsed in the calm years. Stress-test the balance sheet and the supply chain, and give each of the four forces a named owner who tracks it.

Next 90 days. Stand up a standing macro-and-policy watch function that feeds strategy, and build optionality — in financing, sourcing, and routing — so you can move when competitors freeze.

Three boardroom questions

- Which of our plans still assume cheap money, open trade, cheap energy, or light regulation?

- Where are the four forces hitting the same decision at once — and have we modelled that combination?

- Do we have a function that turns macro and policy into strategy, or do we just react to headlines?

Five strategic takeaways

- Treat policy as a strategy input, not a backdrop. It now shapes returns directly.

- Re-underwrite on a higher-for-longer cost of capital. The cheap-money base case is gone.

- Build financing and supply-chain optionality. Optionality is what lets you move while rivals freeze.

- Bring scenario planning back. The benign years let the muscle atrophy.

- Stand up a macro-and-policy watch function. Read the environment ahead of the headlines.

Policy is strategy now

The benign backdrop is not returning soon. The executives who thrive in 2026 will not be the ones who forecast the macro best — no one can — but the ones who build businesses able to take a hit from any of the four forces and keep moving. Policy is strategy now. Plan like it, and you will be making moves while your competitors are still waiting for a forecast that never comes.

Explore the Global Economy & Policy series

This pillar is built from focused, decision-ready clusters under Global Economy & Policy:

- The Hormuz Shock: The 2026 Oil Crisis as a Commercial Risk

- Europe's Digital Rulebook Hardens: DMA, AI Act, and Sovereignty

More clusters publishing soon: The New Cost of Capital · Energy Volatility and the New Cost Base · The Geopolitical Risk Map for Leaders.

FAQs

What is the global growth forecast for 2026? The IMF cut it to 3.1% in its April 2026 outlook, down from a pre-conflict 3.4%, with headline inflation up to 4.4% and downside risks dominating.

Why is the cost of capital higher? Firmer inflation expectations and tighter financial conditions mean central-bank rate cuts are coming slower and shallower than markets assumed, keeping financing costs elevated; the IMF warns a further escalation would add 100–200 basis points to corporate risk premiums.

Is global trade shrinking? Growth is slowing sharply — merchandise trade is set to grow about 1.9% in 2026, down from 4.6% in 2025 — as tariffs and fragmentation bite, with greenfield projects in exposed sectors down about 25% in 2025.

What should executives actually do? Re-underwrite plans on the new baseline, build financing and supply-chain optionality, restore scenario planning, and create a standing macro-and-policy watch function.

Sources: IMF World Economic Outlook (April 2026); WTO Global Trade Outlook (March 2026); UNCTAD Global Investment Trends Monitor / Global Trade Update (2026). Figures should be re-verified against the latest source at publication.